The Federal Reserve just held rates steady at 3.50%-3.75% in its first meeting under new Chair Kevin Warsh, and they're already signaling at least one rate hike before year-end. For churches planning renovations, launching capital campaigns, or just trying to keep the lights on, this isn't abstract economic news. It has real consequences for real ministries starting right now.

I spent last week reviewing operational budgets with three mid-size churches — somewhere in the 500 to 1,200 weekly attendance range — and every single one had the same blind spot: their 2026 budget assumptions were built on 2024's interest rate environment. One church administrator in Charlotte had penciled in a $2.8 million sanctuary renovation assuming a construction loan around 5.5%. That same loan today? The bank quoted 7.25%, adding roughly $340,000 to the total project cost.

But the interest rate story goes deeper than loan payments. When household budgets tighten — which happens when mortgage rates stay elevated and credit card interest compounds — giving patterns shift in predictable ways. Churches that actually track their donation data closely (and most don't) see it first in the reduction of one-time gifts, then in decreased participation in special offerings, and eventually in lower regular tithes.

The hidden cascade: How rate changes ripple through church operations

Most church leaders think about interest rates in terms of their building fund or mortgage refinancing. That's the obvious part. What catches churches off guard is how rate changes ripple into areas that have nothing obvious to do with borrowing.

Start with your donor base. Higher rates mean higher mortgage payments for your members. Anyone with a variable-rate mortgage or HELOC just saw their monthly payment jump. Those planning to refinance are stuck. According to Reuters' coverage of the Fed's latest guidance, sustained higher rates are likely through at least Q3 2026. That family giving $400 monthly might quietly drop to $300 when their mortgage payment climbs by $250.

Then there's the vendor side. Your HVAC contractor, sound system installer, parking lot crew — they're all financing equipment and inventory at higher costs, and those costs get passed along. One facilities manager showed me quotes for the same parking lot resurfacing job: $47,000 in January 2025, $52,500 this spring. Same scope, same contractor.

The sneakier impact is volunteer availability. When household budgets squeeze, people pick up side jobs or extra shifts. That reliable Tuesday morning crew that handles facility maintenance? Half of them just became unavailable because they need the extra income.

Building your rate-resistant budget framework

Volatility segmentation

Simplify your church’s day-to-day operations.

Parshly helps you organize events, track donations, and engage your congregation—all in one place.

- Centralized member management

- Donation tracking & reporting

- Volunteer scheduling & notifications

No credit card required

| Tier | Details |

|---|---|

| Tier 1 (Fixed/Essential): | Staff salaries, insurance, basic utilities, minimum debt service. This should represent 60-65% of your budget. These items don't move much with interest rates. |

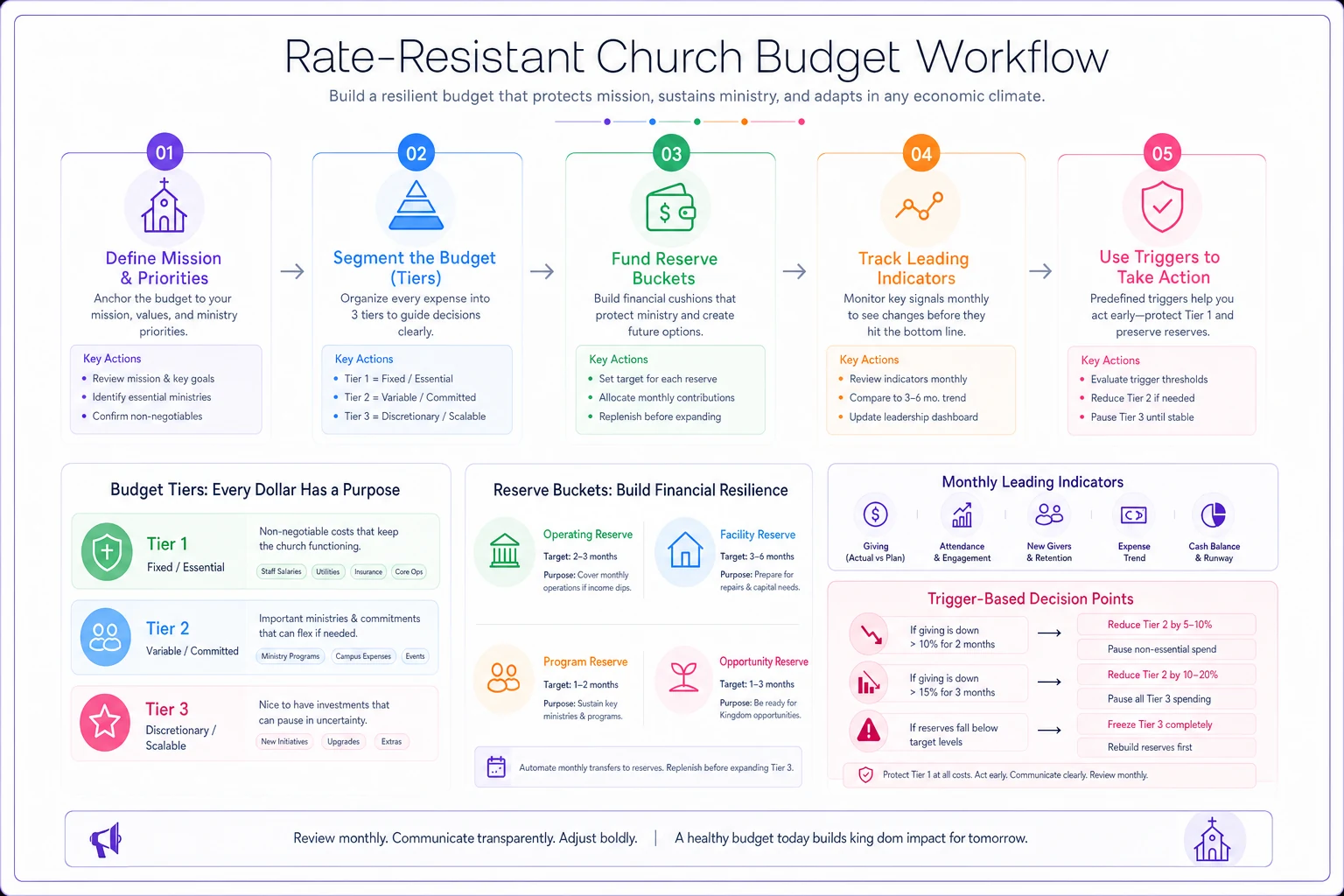

| Tier 2 (Variable/Committed): | Program expenses, discretionary staff, facility improvements, mission support. Usually 25-30% of budget. These flex with giving patterns but have some commitment lag. |

| Tier 3 (Discretionary/Scalable): | New initiatives, equipment upgrades, expanded programs, additional mission work. The remaining 10-15%. This is your adjustment layer. |

When rates rise and giving softens, protect Tier 1, reduce Tier 2 by 10-20%, and potentially pause Tier 3 entirely. The churches that struggle try to cut evenly across all categories, which usually backfires when essential services take the hit.

Multiple reserve strategies

Forget the generic "3-6 months of expenses" rule. In a rate-volatile environment, you need targeted reserves:

-

Operating Reserve 2 months of Tier 1 expenses

-

Facility Reserve $25-30 per square foot of building space

-

Program Reserve 15% of annual Tier 2 budget

-

Opportunity Reserve Variable, but ideally around 5% of annual budget

An 800-member church with a 35,000 square foot facility should maintain roughly $275,000 in operating reserves, $900,000 in facility reserves, $80,000 in program reserves, and $50,000 in opportunity reserves. That's over $1.3 million total. Most churches are sitting on $200,000 or less.

The facility reserve matters more than people realize when rates are high, because emergency repairs can't wait for better financing terms. One church delayed a roof repair by six months hoping rates would drop. That $85,000 repair became a $140,000 replacement after water damage spread.

Here's a quick visual of the budgeting workflow.

Use this to walk your leadership team through trigger points and reserve targets.

Protecting your capital campaign from rate shock

Capital campaigns planned in 2024's rate environment need immediate reassessment. Not cancellation — reassessment. The math has fundamentally changed.

Pledge reliability, campaign duration, and project phasing are all shifting. A three-year campaign that made sense at 5% interest might need to become a five-year campaign at 7.5%. The total raised might be similar, but the timeline and cash flow patterns will look completely different.

Pledge fulfillment assumptions also need updating. Historical fulfillment rates typically run 85-92% for well-run campaigns, but they drop by roughly 5-8 percentage points for every 1% increase in average mortgage rates in your community. If your area moved from 6% to 7.5%, expect fulfillment to fall from around 90% to somewhere near 78%.

Adjusting campaign strategy mid-stream

Extended pledge periods. Instead of three-year pledges, offer five-year options. The monthly amount drops, which makes it easier for donors even if their total capacity has decreased.

Bridge funding partnerships. Partner with sister churches or denominational funds for 18-24 month bridge loans at below-market rates. Several denominations have emergency facility funds specifically for this.

Scope flexing. Design your project in true phases, not just construction stages. Phase 1 covers structural necessities. Phase 2 adds functionality. Phase 3 handles aesthetic improvements. If giving softens, you complete Phase 1 and pause.

The giving pattern shifts nobody talks about

Churches track total giving obsessively but miss the composition changes that actually predict future problems. When rates rise, giving doesn't just decrease — it restructures.

Online giving percentage tends to increase even as total online dollars fall. Committed givers maintain their automated giving while discretionary givers quietly reduce or stop. One church saw online giving jump from 45% to 62% of total giving, which they initially took as a good sign. Then they realized total giving had dropped 18% — the online percentage grew because check and cash giving had cratered.

Estate gifts tend to accelerate in high-rate environments. Older donors with fixed-rate debt and solid investment portfolios often increase giving when they sense their church is under financial pressure. The problem is estate gifts are lumpy and unpredictable. You might receive $200,000 one quarter and nothing for the next three.

Designated giving also shifts toward the general fund. When household budgets tighten, donors want more visibility into where their remaining dollars go. That missions fund receiving $8,000 monthly might drop to $3,000, with some donors redirecting to general operations because they're worried about staff.

Operational adjustments that actually work

Energy audits become worth it. With higher borrowing costs, efficiency improvements that wouldn't pencil out at 4% interest suddenly make sense at 7%. LED conversion, HVAC scheduling, and insulation upgrades often pay back in 18-24 months now. One church reduced monthly utilities from $4,800 to $3,100 with $28,000 in improvements — roughly a 19-month payback.

Prioritize LED conversions and other measures with the shortest payback periods.

Volunteer coordination needs more depth. When volunteers pick up extra work elsewhere, your management approach has to get more sophisticated. Instead of assuming weekly availability, build roster depth. If you need 12 volunteers for children's ministry, recruit 18 and rotate. More coordination work upfront, but far better than scrambling every Sunday.

Payment timing matters more than it looks. Shifting from monthly to annual payments for insurance, software subscriptions, and service contracts often produces 8-12% discounts. That's basically free money when rates are at 7%. One church saved $14,000 annually just by prepaying six vendor contracts.

When member engagement becomes financial resilience

Pressure creates a genuine opening to build proper member engagement systems with defined stages and clear handoffs. Not primarily because engagement systems increase giving — though they often do — but because they reduce operational costs that most churches don't even notice.

A well-designed engagement system means new members get integrated faster, cutting the cost of maintaining attendance through inefficient programming. Volunteer recruitment becomes systematic instead of desperate. Pastoral care happens proactively, reducing the crisis interventions that quietly drain staff bandwidth and budget.

Churches with defined engagement paths spend roughly $42 per new member on integration. Churches without systems spend closer to $180, through higher dropout rates and scattered programming. That $138 difference across 50 new members annually is nearly $7,000 in saved operational cost — real money when every line item is being scrutinized.

Technology decisions in a high-rate environment

This might seem like a bad time to invest in technology, but the ROI math has actually shifted in favor of the right solutions. When borrowing costs are high, operational efficiency gains that don't require capital become more valuable, not less.

The key is choosing technology that consolidates existing costs rather than adding new ones. A church management platform combining donation processing, volunteer scheduling, facility booking, and member database might run $400 monthly but eliminate $600 in separate subscriptions plus 20 hours of monthly staff time. At $20 per hour, that's another $400 in monthly labor savings.

What doesn't work: buying technology hoping it will increase giving. What does work: platforms that measurably reduce operational complexity. The distinction matters because one is speculation and the other is calculable.

Preparing for the next Fed move

The Fed's signal about potential rate increases later in 2026 is operational planning intelligence, not just economist commentary. Every quarter you wait to adjust costs real money and narrows future options.

Start with a rate stress test. Take your current budget and model three scenarios: rates stay flat, rates increase 0.5%, and rates increase 1%. For each scenario, identify your break points. At what giving level do you need to cut staff? Defer maintenance? Reduce programs? Knowing those thresholds lets you build trigger plans instead of panic responses.

Then work on diversifying income streams. Facility rentals, fee-based programs like childcare or counseling, and small social enterprises can provide stable income that doesn't track member giving. One church launched a coffee shop that generates around $3,500 monthly in profit — enough to cover their increased loan payments from recent rate hikes.

Build relationships with multiple lenders now, before you need them. Churches with existing banking relationships and clean financial records can often negotiate rates 0.5-1% below posted rates. On a $500,000 loan, that's roughly $30,000 in interest over five years.

Final thoughts

The churches that hold up during rate volatility aren't always the ones with the biggest budgets or the most generous congregations. They're the ones with operational discipline and realistic planning horizons.

Every church administrator wants to believe their congregation is uniquely resilient — that members will maintain giving despite outside economic pressure. Maybe that's true. But hope isn't a strategy.

The practical reality is that church budgeting during interest rate changes requires more than adjusting a few line items. It means rethinking how you structure reserves, phase projects, engage members, and use technology for efficiency rather than aspiration.

The Fed's message was clear: rates aren't dropping soon. Your operational response needs to match that clarity — systematic adjustment, not wishful thinking. Start with the budget segmentation, move to reserve building, then tackle your capital campaign assumptions. Do it this quarter. In a high-rate environment, delay is one of the most expensive decisions you can make.

The churches that hold up during rate volatility aren't always the ones with the biggest budgets or the most generous congregations. They're the ones with operational discipline and realistic planning horizons.

Every church administrator wants to believe their congregation is uniquely resilient — that members will maintain giving despite outside economic pressure. Maybe that's true. But hope isn't a strategy.

The practical reality is that church budgeting during interest rate changes requires more than adjusting a few line items. It means rethinking how you structure reserves, phase projects, engage members, and use technology for efficiency rather than aspiration.

The Fed's message was clear: rates aren't dropping soon. Your operational response needs to match that clarity — systematic adjustment, not wishful thinking. Start with the budget segmentation, move to reserve building, then tackle your capital campaign assumptions. Do it this quarter. In a high-rate environment, delay is one of the most expensive decisions you can make.

Ready to transform your church management?

Join 500+ churches using Parshly to enhance community engagement, streamline administration, and grow their ministries.